Bitcoin fell 52% from its October 2025 peak of $126K to a February low of $60K. It currently trades around $73K, down 21% year-to-date (as of Mar 20, 2026). Over the same period, software stocks (IGV) are down 18%. The S&P 500 is down 4%.

This article examines what drove the drawdown, maps Bitcoin’s correlation profile across asset classes, and considers what that profile means for how institutional allocators can think about portfolio positioning and risk.

What Triggered the Selloff

The decline began in October. AI infrastructure spending had come under scrutiny as investors questioned whether returns would justify the scale of investment. A more hawkish Fed and tariff uncertainty added to the risk-off mood. Software stocks began softening, and Bitcoin, now structurally linked to the sector, declined alongside them.

This move has been amplified by Anthropic’s January 12 launch of Claude Cowork, an agentic AI system capable of executing complex enterprise workflows without traditional software interfaces. The launch reframed the threat to the sector entirely. The question shifted from whether AI spending would pay off to whether AI success would put traditional software business models under pressure.

Forward P/E ratios compressed significantly as growth expectations reset, and institutional desks de-risked high-beta growth exposures. The same institutional infrastructure that drove ETF inflows during the bull phase transmitted the selloff mechanically into Bitcoin during risk-off. The result: Bitcoin fell 21% year-to-date versus software’s 18%.

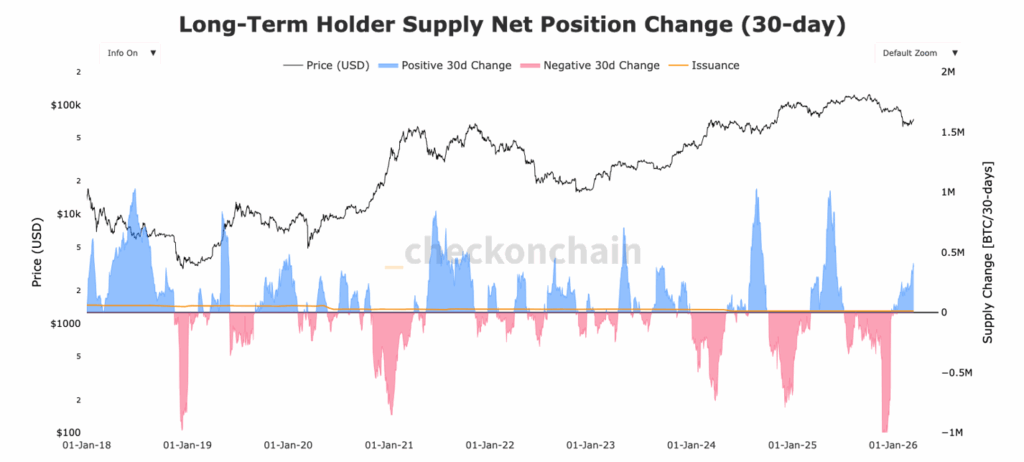

On-chain data reflects the same dynamic. Long-term holder distribution in December 2025 was among the sharpest in Bitcoin’s history, adding a further layer of selling pressure to an already declining market.

Additional factors may have weighed on sentiment, including emerging prediction markets drawing speculative capital away from crypto. Quantum computing concerns also surfaced, though the threat remains theoretical at this stage. These factors were more likely sentiment headwinds than primary drivers of the correction.

Recently, the Iran conflict has added a layer of uncertainty, with Bitcoin showing resilience. Bitcoin initially fell to around $63,000 on the weekend of the US-Israel strikes before recovering toward $71,000 within days, a pattern that closely mirrors prior geopolitical shocks. Historical precedent suggests Bitcoin tends to rebound once markets absorb the initial shock, though whether that holds in a broader and more sustained regional conflict remains an open question.

Bitcoin Asset Correlations

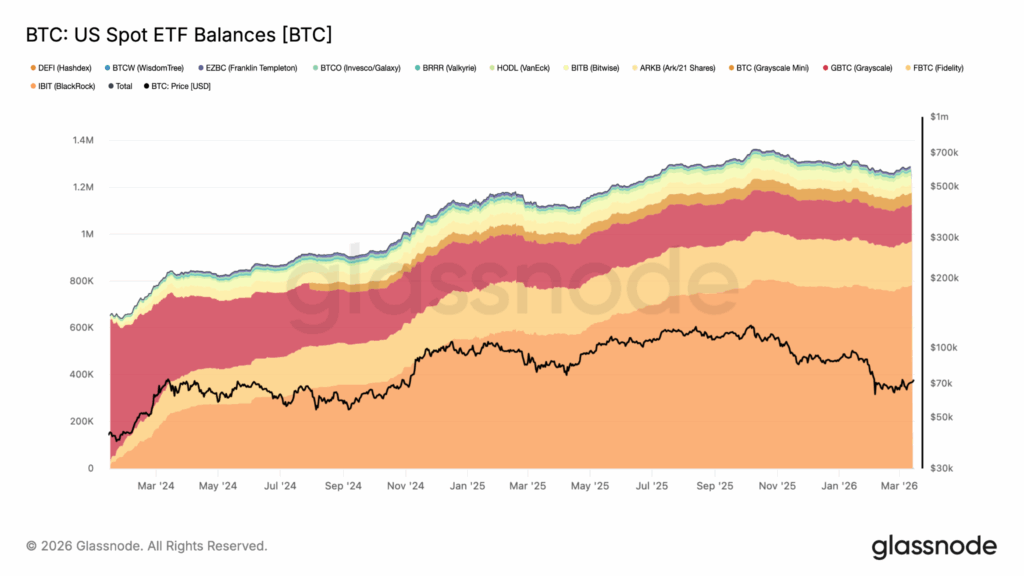

To understand why Bitcoin moved as it did, it helps to understand what the 2024 spot ETF launch actually changed. The $63B in cumulative inflows that followed were not just a validation of Bitcoin as an asset class. They were a structural re-coupling.

Before ETFs, Bitcoin had spent much of 2023 decoupling from tech equities, trading on its own idiosyncratic dynamics as crypto-native participants positioned ahead of the halving and ETF approval. The ETF launch ended that. Once institutional allocators began holding Bitcoin through the same vehicles they use for software and growth equities, Bitcoin became subject to the same risk-on/risk-off framework. When those allocators de-risk, they de-risk everything in the same bucket.

This institutional de-risking was amplified by dynamics in Bitcoin’s derivatives markets, where selling pressure from spot ETFs can trigger outsized price moves.

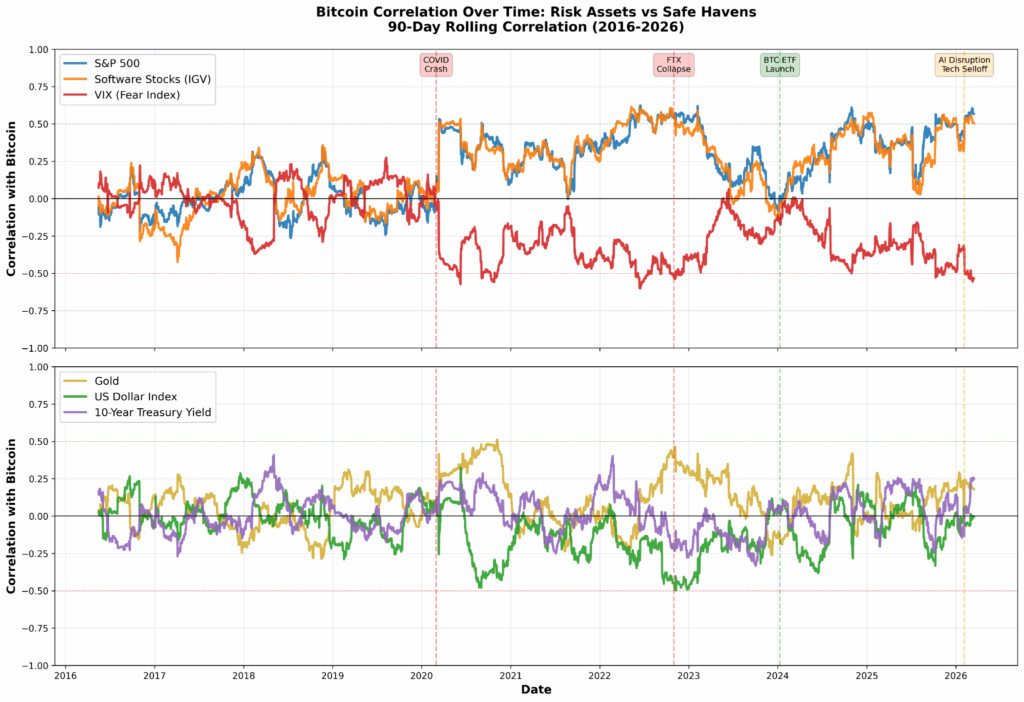

This dynamic is part of a longer evolution. Before 2020, Bitcoin’s correlation with equities was near zero. It was a retail-driven, largely self-contained market. COVID changed that as institutional interest grew and Bitcoin began moving with other risk assets. The FTX collapse in late 2022 caused a temporary break, with Bitcoin decoupling through 2023. The ETF launch in January 2024 closed that window. Institutional allocators now hold Bitcoin alongside software and growth equities in the same portfolios, and appear to manage it the same way.

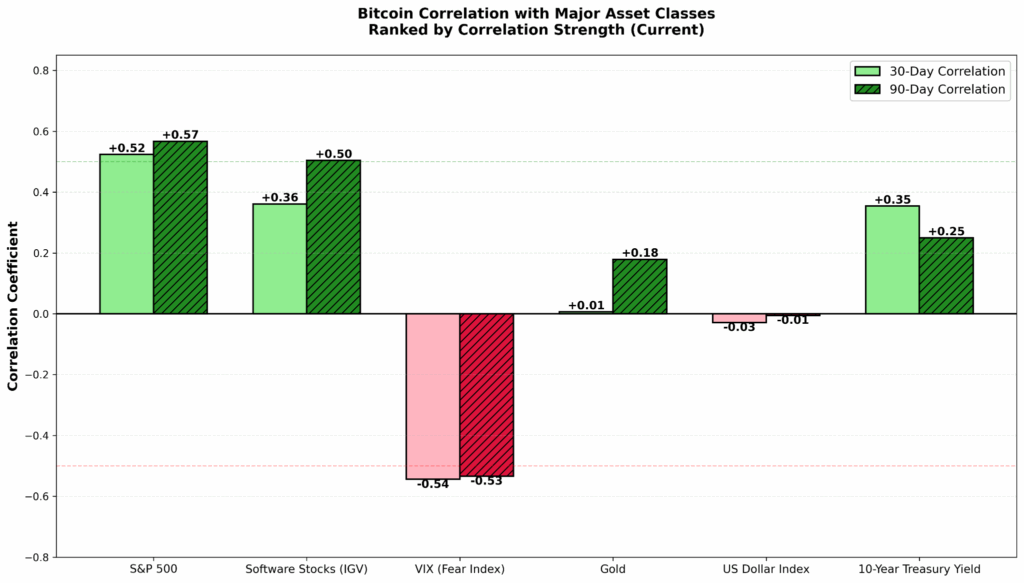

The current numbers reflect that regime. Bitcoin’s 90-day correlation with software (IGV) stands at 0.51, more than double its correlation with gold at 0.18. Correlation with the US dollar is near zero at -0.01, and with treasury yields at +0.25. Bitcoin is moving with risk assets, not with traditional safe havens or currency dynamics.

The VIX correlation makes this most concrete. At -0.53, Bitcoin does not dampen portfolio volatility during stress events. It amplifies it. Gold, by contrast, carries a positive VIX correlation in the same period, behaving as expected during risk-off. Both assets carry a “store of value” narrative. In practice, when fear spikes, they move in opposite directions.

The 30-day window shows early signs of potential divergence. While correlation to the S&P 500 remains elevated at +0.52, the IGV correlation has weakened to +0.36, now nearly matching treasury yields at +0.35. Whether this reflects a temporary shift related to the Iran conflict or the start of a broader decoupling from software equities is too early to determine.

Market Structure Intact

The scale of this drawdown invites the question of whether something structural has broken. The on-chain and flow data suggests it has not.

ETF outflows since the October peak total approximately $8B, yet total BTC held in ETFs declined only 6-7%. Institutional holders absorbed the drawdown rather than exiting the asset class. Long-term holder supply saw a sharp distribution event in December 2025, one of the most significant in Bitcoin’s history in terms of magnitude. Yet as a proportion of circulating supply, long-term holder balances remain elevated. The selling was significant. The base held and since the last week of February we have seen signs of inflows starting to return.

Bitcoin’s supply schedule did not change. Its network did not weaken. The halving cycle continues. What the drawdown reflects is not a repricing of Bitcoin’s fundamental properties but a deleveraging event in the portfolios that hold it. The scarcity that underpins the long-term thesis is structurally intact.

High-Beta Asset or Digital Gold?

The debate around whether Bitcoin is digital gold or a high-beta asset has yet to be settled. Its core properties position it as a potential store of value and more. However, current market pricing tells a different story.

Right now, it is pricing Bitcoin as a high-beta asset. Bitcoin’s correlation regime, the ETF structure, and the institutional portfolio context all point in the same direction. Until something changes that structure (i.e. a sustained decoupling, a shift in how allocators classify the asset, or a reduction in ETF-driven flows), Bitcoin will continue to behave as it has through this drawdown.

The Iran episode offers an early counterpoint worth monitoring. Unlike the tech-driven selloff, Bitcoin’s recovery from that geopolitical shock was swift, consistent with how it has behaved around prior geopolitical events, and hints that its correlation regime is not uniform across all types of market stress.

For active allocators, the correlation regime is the key analytical variable. Whether Bitcoin trades as a tech proxy or a store of value determines its role in the portfolio: a source of concentrated risk that moves in tandem with existing software and growth exposures, or a genuine diversifier with low correlation to traditional assets. That regime is not permanent. It has shifted before, and the conditions that could shift it again (i.e. a reduction in ETF-driven institutional flows, a change in how allocators classify digital assets, or a sustained period of decoupling) are worth monitoring as closely as the price itself.

For long-term investors and believers in the digital gold narrative, that gap between market pricing and Bitcoin’s fundamental properties is precisely where opportunity lies. Mechanical selling driven by institutional de-risking does not change Bitcoin’s fixed supply, its network security, or its other properties that underpin its long-term value thesis. When price disconnects from scarcity for structural rather than fundamental reasons, it reflects a mispricing, not a thesis failure. This is how we approach Bitcoin at Melanion Digital.