In the previous article, we examined how companies like Strategy (formerly MicroStrategy) evolved from traditional operating businesses into sophisticated vehicles for Bitcoin accumulation, ranging from conservative allocation to aggressive accumulation beyond simple corporate speculation.

But one question remained largely unanswered:

Why would investors pay $1.50-$2.00 even more for every $1 of Bitcoin that Strategy or any other Bitcoin Treasury company holds?

On the surface, this seems irrational.

Why not just buy Bitcoin directly and avoid the premium?

While premiums have compressed recently, many Treasury companies still trade at significant multiples of their underlying Bitcoin holdings. Investors continue to pay these premiums willingly. The explanation lies in understanding that these premiums can reflect forward-looking valuations based on anticipated future Bitcoin accumulation, much like investors pay multiples for companies based on projected cash flows.

However, as in any asset class, market enthusiasm can push valuations beyond fundamentals. The recent sharp correction in Bitcoin Treasury mNAV multiples suggests that part of the premium was fueled by hype rather than realistic expectations of future Bitcoin yield. This highlights the importance of understanding what drives these valuations. This article breaks down the concept of the mNAV premium: its mechanics, drivers, and implications for Bitcoin Treasury valuation.

Understanding the mNAV: The Foundation of Bitcoin Treasury Valuation

The multiple of Net Asset Value (mNAV) serves as the primary valuation metric for Bitcoin treasury companies. Two versions exist, each telling a different story about valuation.

The Basic Calculations

Bitcoin NAV = Bitcoin Holdings × Bitcoin Price

Simple mNAV = Market Capitalization ÷ Bitcoin NAV

Fully Diluted mNAV = Fully Diluted Market Cap ÷ Bitcoin NAV

Where Fully Diluted Market Cap = Current Stock Price × (Current Shares + All Potential Converted Shares)

Note: The definition of fully diluted market cap may vary depending on the company. Do your own due diligence on how they report their fully diluted market cap.

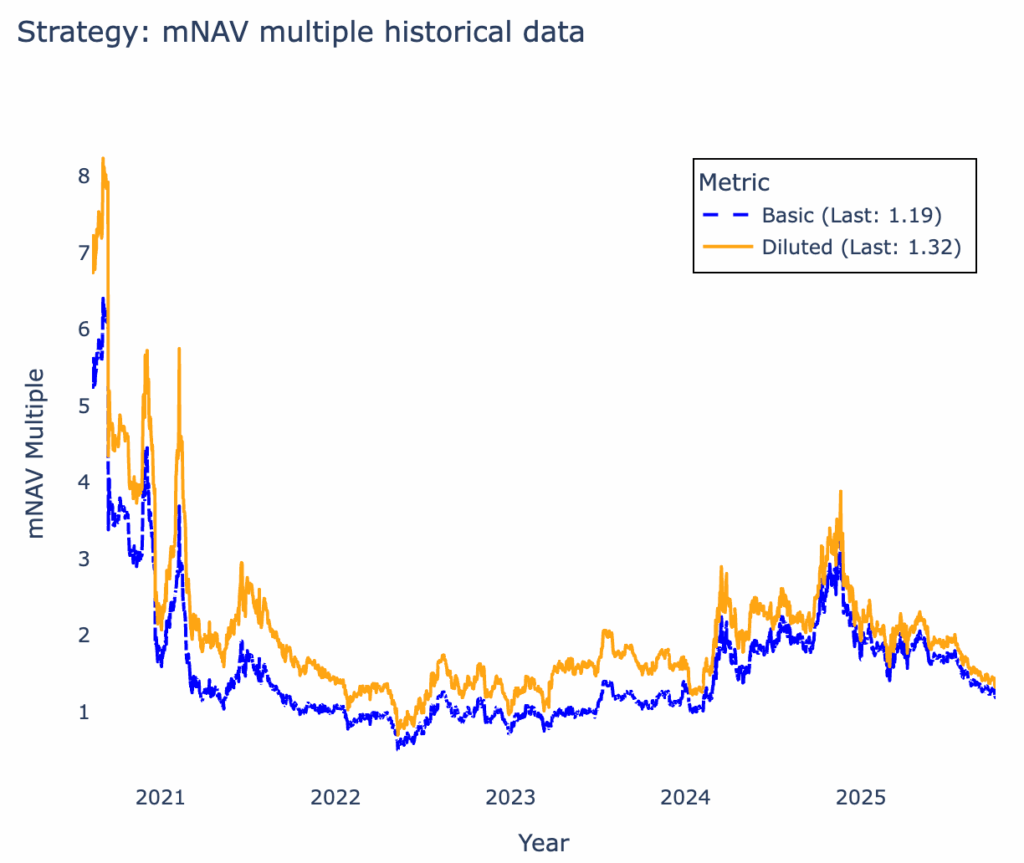

mNAV multiples of Strategy since adoption Bitcoin strategy in 2020 (Own graph. Source: saylortracker.com; 09.10.25)

A Practical Example

Consider a Bitcoin treasury company with:

– 100 million shares outstanding

– Stock price: $15 per share → Market cap: $1.5 billion

– Bitcoin holdings: 10,000 BTC at $100,000 = $1.0 billion

– Outstanding convertible notes that could convert to 25 million additional shares

– Stock options/warrants that could add 5 million more shares

Simple mNAV = $1.5B ÷ $1.0B = 1.5x

Equity investors currently pay $1.50 for every $1 of Bitcoin.

Fully Diluted mNAV = (130M shares × $15) ÷ $1.0B = $1.95B ÷ $1.0B = 1.95x

If all convertibles, options, warrants, etc., convert to shares, investors would effectively pay $1.95 for every $1 of Bitcoin.

Note: The “fully diluted mNAV” usually assumes 100% conversion of all potential shares. This means that, in that metric, the company already considers the Bitcoin as part of its holdings, as in ownership. However, there may be cases where convertible note investors might prefer debt repayment instead of equity conversion.

In a more precise analysis, you could assign a probability of conversion to instruments like convertible notes, based on factors such as the note’s strike price relative to the current share price and the expected future share price, as well as its expiration date.

Why Both Metrics Matter

The simple mNAV shows today’s premium but can be misleading. When companies issue convertible notes to buy Bitcoin, simple mNAV initially falls at constant share price (more Bitcoin, same current share count = increase in Bitcoin per share), making shares seem more attractive to new buyers. However, fully diluted mNAV shows the future reality.

Those convertible notes will likely convert to shares, especially during bull markets. The fully diluted metric accounts for this probable dilution, providing a more conservative and realistic long-term valuation picture.

This distinction becomes important when comparing companies. A company trading at 1.5x simple mNAV with significant convertible debt may actually be more expensive than a company at 1.7x simple mNAV with a clean capital structure, once you consider potential future dilution.

Why Premiums Exist: The Forward-Looking Value Proposition

Premiums exist because investors expect growth in Bitcoin per share, similar to equity investors valuing future cash flows.

The Pure Yield Formula

The key insight is that Bitcoin treasury companies can generate what is called “Bitcoin yield”: increasing Bitcoin per share over a specific period through strategic capital raising. Bitcoin per share refers to the ratio of a company’s Bitcoin holdings relative to its fully diluted shares. An increase in this ratio over time represents the Bitcoin yield.

The total value proposition combines two elements:

Total USD Yield Advantage over Bitcoin = BTC Yield × (1 + BTC Price Appreciation)

For instance, if a company increases its Bitcoin per share by 20% while Bitcoin’s price rises 20%, the total USD yield advantage is 24%.

This 24% advantage over simply holding Bitcoin directly can justify paying a premium for the company’s shares, depending on the investor’s risk preferences, time horizon and portfolio strategies.

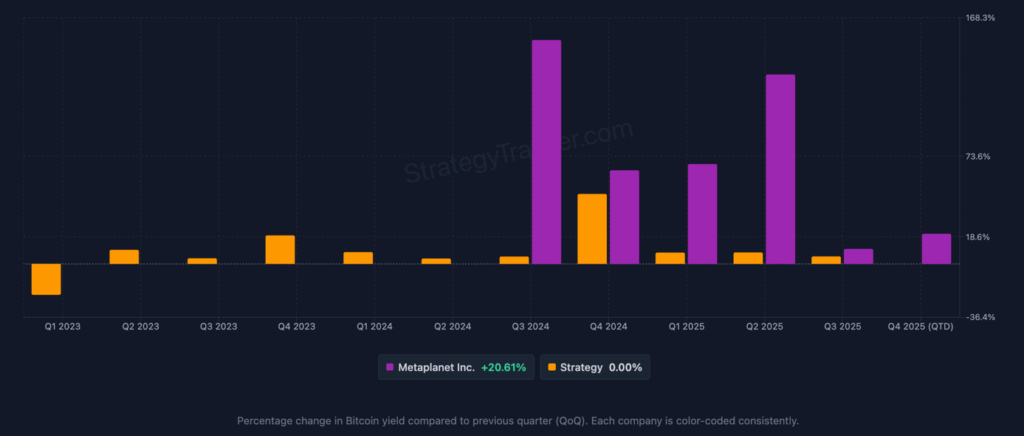

Bitcoin Yield Quarter-over-Quarter: Metaplanet Inc. and Strategy (Source: strategytracker.com; 09.10.2025)

What Drives Premium Levels

Several factors determine the size of premiums that Bitcoin treasury companies can command:

Execution Track Record

Investors pay higher premiums for companies that consistently and rapidly grow their Bitcoin per share, rewarding a proven track record in complex capital strategies. However, there’s a trade-off: smaller companies can achieve this growth more easily, presenting a high-yield but high-risk investment due to their limited track record.

Capital Raising Efficiency

The cost and effectiveness of raising capital directly impacts expected yields. Companies that can access cheap funding (low-interest convertible bonds, premium equity issuances) can generate higher Bitcoin yields.

Regulatory Arbitrage

Premiums also reflect regulatory advantages, such as favorable tax treatment in certain jurisdictions and institutional mandates that restrict direct cryptocurrency purchases, that make Bitcoin treasury companies attractive even when direct Bitcoin ownership is available.

Market Conditions

Bull markets increase premiums as Bitcoin appreciation amplifies the total yield advantage. Bear markets compress premiums as capital becomes scarce and Bitcoin yields harder to achieve.

Management Quality and Competition

Clear strategy communication and transparent reporting build investor confidence, supporting higher premium valuations. The availability of Bitcoin ETFs and other direct exposure methods affects premiums, though regulatory arbitrage often supports premiums even when direct alternatives exist.

Hype

As mentioned in the introduction, there can also be hype around treasury companies, just like in any other industry, where some of the premium might not reflect fundamentals or rational expectations.

Scenario Analysis: When Are Different Premiums Justified?

Using the Pure Yield Formula, we can evaluate what premium levels are reasonable under various scenarios. In the scenarios, we assume a one-year time horizon.

| BTC Yield Per Share | BTC Price Change | Total Yield Advantage | Justified mNAV at 10x P/E |

| 20% | 20% | 24% | 2.4x |

| 20% | 30% | 26% | 2.6x |

| 30% | 20% | 36% | 3.6x |

| 10% | 20% | 12% | 1.2x |

Note: Using 10x P/E as baseline; actual multiples vary based on risk assessment and market conditions

This framework shows that:

- Higher expected Bitcoin yields justify higher premiums

- Bitcoin price appreciation amplifies the total value proposition

- Companies expecting modest yields should trade closer to NAV

Premium Sustainability and Risks

While premiums reflect legitimate value propositions, several factors can cause them to compress or disappear, including market overshoot, where enthusiasm pushes valuations beyond what any realistic Bitcoin yield projection can justify, as recent sharp mNAV corrections across the sector have demonstrated:

Execution and Market Risks

Companies that don’t meet Bitcoin accumulation expectations lose their premiums. As more firms enter the space, standing out becomes harder. In bear markets, raising capital is difficult, which can halt accumulation and force a company’s stock to trade below its net asset value (NAV).

Regulatory Risks

Shifts in tax treatment, institutional regulations, or Bitcoin legal status could eliminate the arbitrage opportunities that support premiums. Changes in how different jurisdictions tax Bitcoin versus equity gains directly impact the economic rationale for these structures.

We’ll explore these risks and additional threats to Bitcoin treasury models in greater depth in a later article in this series.

Conclusion

The mNAV premiums of Bitcoin Treasury companies are not necessarily market anomalies or unjustified. They can reflect nuanced valuations of a company’s ability to generate Bitcoin yield per share while offering regulatory arbitrage benefits. Understanding the Pure Yield Formula and the factors driving execution success helps investors assess whether such premiums are justified or excessive.

The most successful companies will combine steady Bitcoin accumulation with transparent communication and prudent risk management. As the sector matures, more Bitcoin Treasury companies are likely to allocate capital in ways that extend beyond pure accumulation through capital market raises, building organic yield and sustainable growth.

At Melanion Digital, we have demonstrated since 2021 that generating yield on Bitcoin holdings through market-neutral strategies and active treasury management can complement a strategy that solely depends on continuous capital raises. As competition intensifies, such innovative approaches that foster organic growth regardless of market conditions will become increasingly important.

Companies that can sustainably deliver Bitcoin yields above the total return from direct Bitcoin ownership will likely continue to show positive mNAV values. Those that cannot will see their valuations converge toward NAV, or below it if their execution consistently disappoints and the leading Treasury companies may acquire them.

Next in this series: “The Bitcoin Treasury Flywheel: How Self-Reinforcing Cycles Create Value” – exploring the momentum dynamics that amplify both growth and risk.